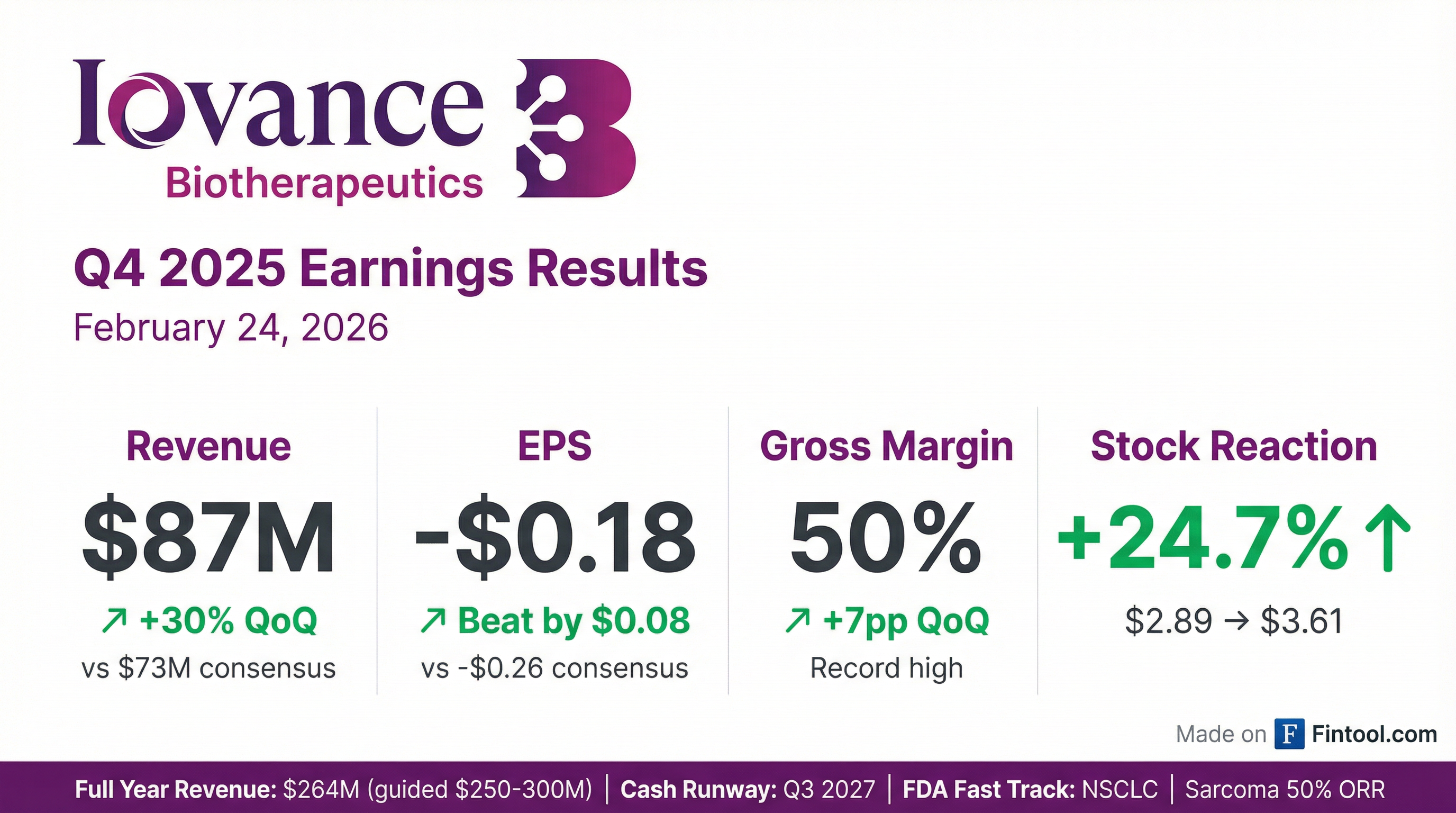

IOVANCE BIOTHERAPEUTICS (IOVA)·Q4 2025 Earnings Summary

Iovance Surges 25% as Amtagvi Beats Big, Sarcoma Data Stuns

February 24, 2026 · by Fintool AI Agent

Iovance Biotherapeutics (NASDAQ: IOVA) reported Q4 2025 results that crushed expectations, driving shares up 24.7% to $3.61. The company delivered ~$87M in total product revenue (30% sequential growth), achieved a record 50% gross margin, and announced unprecedented 50% response rates in soft tissue sarcoma — opening a major new market opportunity .

Did Iovance Beat Earnings?

Yes — Iovance beat on both revenue and EPS with improving profitability metrics.

*Values retrieved from S&P Global

The beat was driven by accelerating Amtagvi demand, improving manufacturing efficiency, and full internalization of production at ICTC. Gross margin expanded to a record 50% in Q4 from 43% in Q3 and 38% a year ago .

"Our operational strength resulted in a robust 30% revenue growth, driven by Amtagvi and our best-ever 50% margin from cost of sales in the fourth quarter." — Dr. Frederick Vogt, Interim CEO

How Did the Stock React?

IOVA surged 24.7% — the largest single-day move in over a year.

The stock has rallied 120% from the 52-week low of $1.64 but remains 39% below the $5.88 high. Today's move reflects investor enthusiasm for the sarcoma data, record margins, and management's confidence in "remarkable growth" for 2026.

What Did Management Guide?

Management did not provide explicit 2026 revenue guidance but signaled it's coming "very soon" :

"Right now we're seeing remarkable growth in the Amtagvi business. We do need to be sure that our projections are well supported, so we're taking some time to do that. It's very early in the year right now, of course, but as I mentioned during the prepared remarks, we're going to be putting guidance out very, very soon." — Dr. Frederick Vogt

Key Financial Guidance:

- Cash Runway: $303M as of December 31, 2025, expected to fund operations into Q3 2027

- Gross Margin: Further improvement expected from manufacturing optimization

- Proleukin Mix: ~17% of revenue long-term, consistent with pricing ratio

What's the Peak Sales Potential?

Management outlined a massive market opportunity across three indications :

"When we talk about layering lung in, I mentioned in the script, that is a $10 billion opportunity, a much larger market to go into. Sarcoma we do see as being equivalent to melanoma, so we do see tremendous potential to be well over $10-$12 billion in the U.S. with Amtagvi." — Dan Kirby, Chief Commercial Officer

What Changed From Last Quarter?

Positive Developments:

-

Gross margin inflection — 50% in Q4 vs 43% in Q3, driven by manufacturing optimization and ICTC internalization

-

Sarcoma breakthrough — 50% confirmed ORR in undifferentiated pleomorphic sarcoma and dedifferentiated liposarcoma (vs <5% with standard of care)

-

FDA Fast Track — Granted for lifileucel in 2L+ NSCLC, supporting potential accelerated approval

-

Community ATC expansion — New community centers contributing to highest-ever quarterly demand

-

Real-world data validation — TANDEM meeting data showed 50%+ ORR in second-line setting, resonating with physicians

Continuing Challenges:

- Still burning cash (~$70-100M quarterly net loss)

- Limited runway (into Q3 2027) requires continued execution

- Stock still well below 2024 highs

What Were the Key Q&A Highlights?

TILVANCE-301 Frontline Melanoma

Analysts asked about potential interim data timing. Management confirmed an early interim ORR read is possible but couldn't commit to 2026 :

"We do have an early interim read in this study... It's in the near term, and we'll be able to do that. We can't really commit to doing that in 2026 right now." — Dr. Frederick Vogt

The benchmark is pembrolizumab monotherapy from KEYNOTE-006 (~30-35% ORR), while Iovance's IOV-COM-202 combination data showed response rates in the 60% range .

Sarcoma Registrational Trial Size

Based on recent FDA approvals in soft tissue sarcoma, management expects 40-patient registrational trial for each subtype :

"Based upon the prior approvals in very soft tissue sarcoma subtypes recently by FDA, approval size for the various subtypes has ranged between 30 patients and 60 patients, but predominantly in the 40-patient range."

Academic vs Community ATC Dynamics

The Q4 acceleration came primarily from academic ATCs, with community centers still ramping :

"For Q4, our base book of business is the academic ATCs, and we saw significant growth in that segment... we have earlier procurement strategies for patients such as BRAF-mutated patients, which make up a significant number of those patients inside of the academic ATCs that we were not previously able to access." — Dan Kirby

Proleukin Ordering Normalization

All three wholesalers ordered in Q4, with reordering already occurring in Q1. The long-term revenue ratio is 17% Proleukin / 83% Amtagvi, consistent with the pricing ratio .

International Margins

Manufacturing for ex-U.S. launches will be from Philadelphia (ICTC), with no added facilities needed. Importantly, no ex-U.S. price has been negotiated yet, positioning Iovance favorably vs. Most-Favored-Nation concerns .

Pipeline and Catalysts Ahead

Upcoming Data Presentations: Sarcoma data expected at a major medical congress (ASCO or ESMO) in 2026 .

Beat/Miss History (Last 8 Quarters)

*Values retrieved from S&P Global

Key Management Quotes

On Commercial Momentum:

"After a considerable increase in fourth quarter demand for Amtagvi, enrollment volumes in 2026 are accelerating within our broad and continuously expanding network of both academic and community Authorized Treatment Centers."

On Sarcoma Opportunity:

"These extraordinary results are what I hoped and believed I would see TIL therapy do in solid tumor cancers when I chose to leave academic medicine to join Team Iovance. I am heartened by this major opportunity for patients and the future of TIL therapy." — Dr. Brian Gastman

On Path to Profitability:

"In 2026, we are laser-focused on maximizing shareholder value, ending dilution, and supercharging future profitability."

Key Takeaways

-

Blowout quarter — 30% sequential revenue growth with record 50% gross margin demonstrates commercial acceleration and operational leverage

-

Sarcoma game-changer — 50% ORR in a disease with <5% standard-of-care response rates opens a market equivalent to melanoma ($1B+)

-

NSCLC catalyst approaching — $10B opportunity with FDA Fast Track, potential 2H 2027 launch

-

Guidance imminent — "Very soon" with "remarkable growth" expectations suggests significant 2026 upside

-

Cash remains watch item — $303M with runway into Q3 2027; execution critical to avoid dilution

Bottom Line: Iovance delivered a transformational quarter that resets the investment narrative. The 50% sarcoma ORR data, combined with record margins and accelerating Amtagvi demand, validates the TIL platform's potential across solid tumors. With NSCLC and sarcoma adding $11B+ in addressable market to the existing melanoma franchise, the path to a multi-billion-dollar cell therapy leader is becoming clearer. The 25% stock move suggests the market is finally pricing in execution — but with cash runway into Q3 2027, sustained performance is essential.